.svg)

The universal registration document complements a series of initiatives, spearheaded by integrated reporting and the DPEF. These initiatives are all part of the convergence of financial and non-financial reporting, aimed at promoting a better understanding of value creation and its sharing by companies, which are key to the sustainability of economic actors.

Universal registration document: communicating risks more effectively

The universal registration document (URD) has been required since July 21, 2019, for prospectuses submitted for approval. It introduces a change in the presentation of risks, pursuant to Article 16 of Prospectus Regulation 3.

Issuers are invited to present their financial and non-financial strategies in a more readable manner. They must now only take into account significant risks specific to their business, in a section dedicated to risks, covering all risks, including non-financial risks. The selected risks, up to a maximum of 15 (in accordance with Article 7 of the Prospectus Regulation), must be ranked and classified by category and sub-category of risk factors (up to a maximum of 10). The most significant risk factors must be mentioned at the beginning of the list for each category. In its assessment, the issuer may use a qualitative scale specifying whether the risk is low, medium, or high.

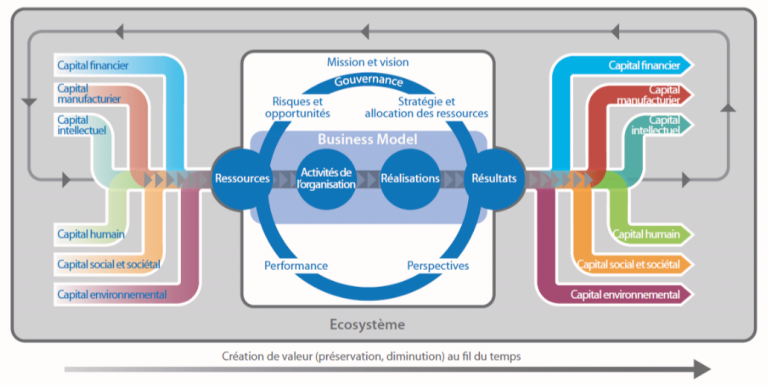

Towards a comprehensive assessment of corporate performance

In integrated reporting, the correlation between financial capital and manufacturing, intellectual, human, societal, and environmental capital enables value creation over time. It identifies risks—but also opportunities—that are both financial and non-financial in nature. The reciprocity of financial and non-financial factors. The reciprocity of financial and non-financial factors is the cornerstone of integrated thinking.

This perspective on financial and non-financial risks allows for a better assessment of the company's prospects for sustainability.

In a sign of the times, in April 2019, the Securities and Exchange Commission indicated that the reporting system should evolve to include information on intangible assets such as intellectual property and human capital.

These developments are a step in the right direction—toward the growing importance of ESG criteria in assessing companies’ overall performance, particularly to meet investors’ needs. The goal? “To ensure that companies fully take into account the interests of society, the planet, and all of their stakeholders,” as Dominic Barton, president of the International Integrated Reporting Council, noted regarding the evolution of integrated reporting around the world.

For decades, finance has relied on key performance indicators. The DPEF encourages companies to use KPIs to steer policies implemented to reduce and avoid identified non-financial risks. Many companies have changed the frequency with which they collect certain financial data in order to align with this approach. This is encouraging. It remains to be seen whether, in the near future, non-financial KPIs will feature on the agenda of executive committee meetings in the same way as economic KPIs. When we reach that point, financial and non-financial considerations will have fully and completely converged.

Need help with your ESG reporting? Check out our ESG and CSRD software, Tennaxia.

Want to learn more? Check out our article on non-financial reporting.

Photo credit: Vitaly Gariev